By Surya Padhi, EA, CAA | Sure Financial & Tax Services

When most people think about taxes, they assume that every dollar they receive is taxable. However, the Internal Revenue Code includes several types of income that may be excluded from federal taxation under specific circumstances.

Understanding these tax-free income opportunities can help individuals, families, retirees, and business owners make smarter financial decisions and reduce unnecessary tax liability.

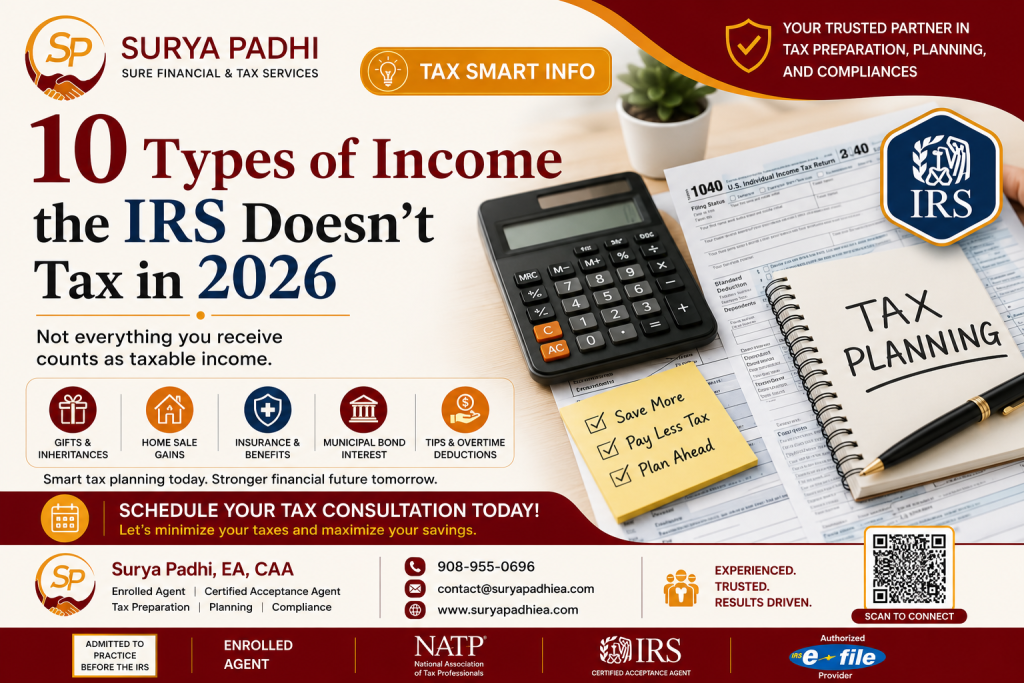

In this guide, we’ll explore 10 common types of income that the IRS generally does not tax in 2026.

1. Gifts

Money or property received as a gift is generally not taxable to the recipient.

For 2026, individuals can receive gifts without reporting them as taxable income. If a gift exceeds the annual exclusion amount, the giver—not the recipient—may be required to file a gift tax return.

Tax Planning Tip:

Large family wealth transfers can often be structured to minimize future estate taxes while remaining completely tax-free to beneficiaries.

2. Inheritances

Most inheritances received from estates are not subject to federal income tax.

Whether you inherit cash, investments, or real estate, the inheritance itself is generally tax-free. However, future income generated from inherited assets may be taxable.

Tax Planning Tip:

Inherited assets often receive a “step-up in basis,” which can significantly reduce future capital gains taxes.

3. Life Insurance Death Benefits

Life insurance proceeds paid to beneficiaries are generally exempt from federal income tax.

This makes life insurance one of the most effective tools for wealth preservation and family financial protection.

Tax Planning Tip:

Proper beneficiary designations help ensure tax-efficient transfer of wealth to loved ones.

4. Qualified Roth IRA Distributions

Qualified Roth IRA withdrawals can be completely tax-free.

To qualify:

- Account must be open for at least 5 years.

- Account holder must be age 59½ or older (or meet certain exceptions).

Tax Planning Tip:

Roth accounts can be powerful retirement planning tools because qualified distributions are tax-free.

5. Child Support Payments

Child support payments are not taxable income to the recipient.

Likewise, the payer cannot claim a tax deduction for child support payments.

Tax Planning Tip:

Many taxpayers mistakenly confuse child support with alimony, which follows different tax rules.

6. Home Sale Gain Exclusion

Homeowners may exclude a significant portion of gain from the sale of their primary residence.

Exclusion Limits:

- Up to $250,000 for single filers

- Up to $500,000 for married couples filing jointly

To qualify, you generally must have owned and lived in the home for at least two of the last five years.

Tax Planning Tip:

Strategic timing of home sales can potentially eliminate thousands of dollars in capital gains taxes.

7. Municipal Bond Interest

Interest earned from many municipal bonds is exempt from federal income tax.

In some cases, interest may also be exempt from state income tax if the bonds were issued by your home state.

Tax Planning Tip:

Municipal bonds are often attractive for high-income taxpayers seeking tax-efficient investment income.

8. Workers’ Compensation and Certain Disability Benefits

Workers’ compensation benefits are generally tax-free.

Certain disability payments may also be tax-free when premiums were paid using after-tax dollars.

Tax Planning Tip:

The tax treatment of disability income depends heavily on how the policy premiums were funded.

9. Qualified Tip Income Deduction (2025–2028)

Recent tax legislation provides eligible workers with potential deductions related to qualified tip income.

Certain income thresholds and phase-out limitations apply.

Tax Planning Tip:

Service industry workers should maintain accurate tip records to maximize available tax benefits.

10. Qualified Overtime Pay Deduction (2025–2028)

Certain overtime compensation may qualify for special tax treatment under current legislation.

Eligibility requirements, income limits, and phase-outs apply.

Tax Planning Tip:

Employees should review payroll records carefully to determine eligibility for available deductions.

Additional Sources of Tax-Free Income

Several other valuable tax-free benefits may include:

- Health Savings Account (HSA) withdrawals used for qualified medical expenses

- Employer-paid health insurance benefits

- VA disability benefits

- Long-term care insurance benefits

- Certain educational assistance programs

Important State Tax Considerations

While many income exclusions apply for federal tax purposes, state tax rules may differ significantly.

Some states tax income that is excluded federally, while others provide additional exemptions.

Always review both federal and state tax rules before making major financial decisions.

How Tax Planning Can Help You Keep More of Your Money

The tax code contains numerous opportunities to legally reduce taxes and build wealth. Understanding which income sources are taxable—and which are not—is an essential part of any financial plan.

At Sure Financial & Tax Services, we help individuals, families, retirees, and business owners develop tax-efficient strategies that align with their long-term goals.

Need Professional Tax Guidance?

Whether you’re planning for retirement, selling a home, managing inherited assets, or looking to reduce your overall tax burden, our team can help.

Schedule a consultation today and discover opportunities to keep more of what you earn.

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

📧 contact@suryapadhiea.com

🌐 www.suryapadhiea.com

Disclaimer: This article is for informational purposes only and should not be considered legal, tax, or financial advice. Consult a qualified tax professional regarding your specific circumstances.