By Surya Padhi, EA, CAA | Sure Financial & Tax Services

Every year, millions of Americans file their tax returns accurately and never hear from the IRS again. However, certain mistakes, omissions, or unusual reporting patterns can increase the likelihood of receiving an IRS notice or having your return selected for further review.

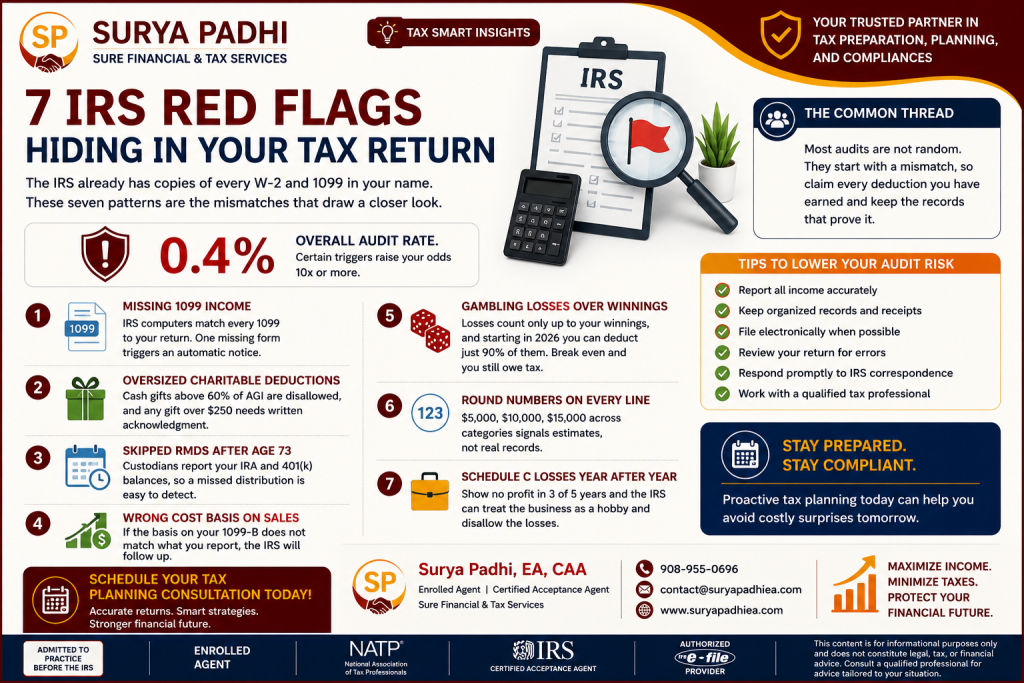

While the overall IRS audit rate remains relatively low—around 0.4% for individual returns—certain reporting errors can significantly increase your chances of attracting IRS attention.

The good news? Most IRS notices and audits are preventable with accurate recordkeeping and careful tax preparation.

In this guide, we’ll discuss seven common IRS red flags and how you can avoid them when filing your 2026 tax return.

1. Missing 1099 Income

One of the most common reasons taxpayers receive IRS notices is failing to report all taxable income.

Financial institutions, employers, brokerage firms, and payment processors send copies of Forms 1099 directly to the IRS. The IRS uses automated matching systems to compare these forms against your tax return.

Common forms include:

- Form 1099-NEC

- Form 1099-MISC

- Form 1099-K

- Form 1099-INT

- Form 1099-DIV

- Form 1099-B

- Form SSA-1099

- Form 1099-R

If even one form is omitted, the IRS may issue a CP2000 notice proposing additional tax.

How to Avoid This Red Flag

✔ Wait until you’ve received all tax documents before filing.

✔ Review your IRS Wage and Income Transcript if you’re unsure whether you’ve received every form.

✔ Double-check brokerage and online payment platform statements.

2. Unusually Large Charitable Contributions

Charitable donations are valuable tax deductions—but unusually large deductions compared to your income may attract additional scrutiny.

For cash contributions:

- Donations generally cannot exceed IRS percentage limitations based on Adjusted Gross Income (AGI).

- Contributions of $250 or more require a contemporaneous written acknowledgment from the charitable organization.

Non-cash donations may also require qualified appraisals and additional documentation depending on value.

Best Practice

Maintain:

- Donation receipts

- Bank records

- Acknowledgment letters

- Appraisals (when required)

Proper documentation is your best defense if the IRS requests support.

3. Missing Required Minimum Distributions (RMDs)

Many retirees are required to begin taking Required Minimum Distributions (RMDs) from certain retirement accounts beginning at the applicable IRS age.

The IRS receives annual reporting from financial institutions regarding retirement account balances and distributions.

Failing to take an RMD may result in penalties unless corrected promptly.

Retirement Accounts Subject to RMD Rules

- Traditional IRA

- SEP IRA

- SIMPLE IRA

- Traditional 401(k)

- 403(b)

Roth IRAs generally do not require lifetime RMDs for the original owner.

Tax Planning Tip

Review your retirement accounts each year to ensure required distributions are taken before the IRS deadline.

4. Incorrect Cost Basis Reporting

Selling investments without accurately reporting cost basis is another common trigger for IRS correspondence.

Brokerage firms report stock sales on Form 1099-B, including:

- Purchase price (when available)

- Sales price

- Gain or loss

If your reported gain differs significantly from IRS records, the IRS may request clarification.

Keep Records Of

- Purchase confirmations

- Dividend reinvestments

- Stock splits

- Corporate actions

- Inherited asset basis adjustments

Good recordkeeping helps ensure capital gains are calculated correctly.

5. Claiming Gambling Losses Improperly

Gambling winnings are generally taxable and must be reported as income.

While gambling losses may be deductible under certain circumstances, they are subject to IRS limitations and documentation requirements.

You should maintain:

- Win/loss statements

- Casino records

- Betting slips

- Bank statements

- Gambling diary

Without proper documentation, the IRS may disallow claimed losses.

6. Excessive Round Numbers

Tax returns filled with perfectly rounded numbers may raise questions because they can suggest estimates rather than actual records.

Examples include:

- $5,000 Office Expenses

- $10,000 Advertising

- $15,000 Travel

- $20,000 Supplies

While rounded amounts aren’t prohibited, repeated estimates across multiple categories may increase scrutiny.

Best Practice

Maintain detailed bookkeeping and report actual expenses whenever possible.

Accounting software can help ensure greater accuracy.

7. Reporting Business Losses Year After Year

Many small businesses experience losses during startup years. However, reporting continuous losses over an extended period may cause the IRS to question whether the activity is truly operated for profit.

The IRS may classify an activity as a hobby if it lacks a genuine profit motive.

When this happens:

- Business deductions may be limited.

- Losses may be disallowed.

- Additional tax may be assessed.

Demonstrating a Profit Motive

Maintain:

- Business plans

- Marketing efforts

- Separate business bank accounts

- Financial statements

- Profit improvement strategies

Showing that you actively manage your business like a business—not a hobby—helps support your deductions.

Additional IRS Audit Triggers to Watch For

Besides the seven common red flags above, taxpayers should also pay close attention to:

Cryptocurrency Transactions

Digital asset transactions—including sales, exchanges, staking rewards, and certain payments—may create taxable events. Be sure to report all required cryptocurrency activity accurately.

Home Office Deductions

Home office deductions are available only when IRS requirements are met. Keep detailed records and ensure the space is used regularly and exclusively for business.

Large Cash Transactions

Businesses receiving significant cash payments may have additional reporting requirements under federal law.

Foreign Financial Accounts

U.S. taxpayers with foreign bank accounts or specified foreign financial assets may need to file additional information returns, such as FBAR or Form 8938.

Tips to Reduce Your Audit Risk

While no one can guarantee an audit-free return, these best practices can reduce your chances of receiving an IRS notice:

- Report all income accurately.

- Keep organized records and receipts.

- File electronically when possible.

- Review your return for errors before filing.

- Respond promptly to IRS correspondence.

- Work with a qualified tax professional if your return is complex.

Why Professional Tax Preparation Matters

The IRS increasingly relies on sophisticated data matching systems to identify inconsistencies. Even honest mistakes can trigger notices or delays.

Working with an experienced tax professional helps ensure:

✔ Accurate income reporting

✔ Proper deduction documentation

✔ Retirement distribution compliance

✔ Correct capital gains calculations

✔ Tax-saving opportunities without unnecessary audit risk

Schedule Your Tax Planning Consultation

Whether you’re filing an individual return, managing a business, or planning for retirement, proactive tax planning can help you reduce errors, maximize deductions, and stay compliant with IRS rules.

At Sure Financial & Tax Services, we help individuals, families, investors, and business owners prepare accurate tax returns while identifying strategies to legally minimize taxes.

Our services include:

✔ Individual Tax Preparation

✔ Business Tax Returns

✔ IRS Notice Assistance

✔ Tax Planning & Projections

✔ Retirement Tax Planning

✔ Capital Gains & Investment Tax Planning

✔ Small Business Tax Consulting

Contact Us Today

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 Phone: 908-955-0696

📧 Email: contact@suryapadhiea.com

🌐 Website: www.suryapadhiea.com

Stay Compliant. Maximize Your Deductions. Minimize Your Tax Burden.

Schedule your consultation today and gain confidence that your tax return is accurate, complete, and optimized for your financial goals.

Disclaimer

This article is for informational purposes only and should not be considered legal, tax, or financial advice. IRS rules are subject to change, and every taxpayer’s situation is unique. Consult a qualified tax professional before making tax-related decisions.