By Surya Padhi, EA, CAA | Sure Financial & Tax Services

Saving for retirement is one of the smartest financial decisions you can make, but choosing the right retirement account can be confusing. Should you contribute to your employer’s 401(k), open a Roth IRA, or invest in a Traditional IRA?

Each account offers unique tax advantages, contribution limits, and withdrawal rules. Understanding these differences can help you maximize your retirement savings while minimizing your lifetime tax burden.

In this guide, we’ll compare the three most popular retirement accounts and explain how to decide which one fits your financial goals.

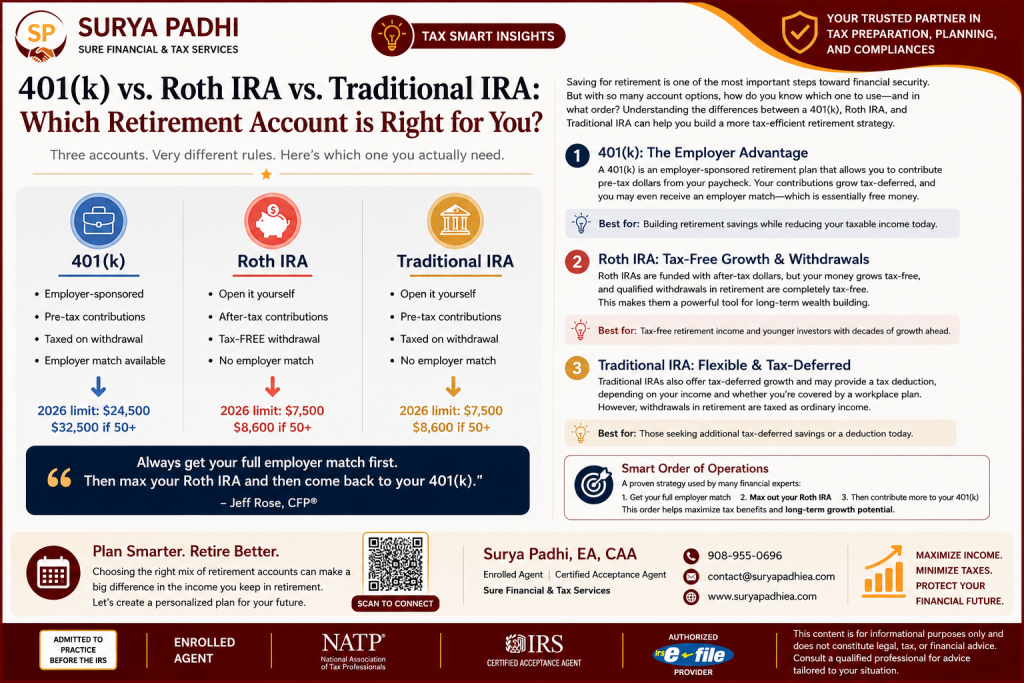

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their salary before taxes (traditional 401(k)) or after taxes (Roth 401(k), if offered).

Key Benefits

- Employer-sponsored retirement plan

- Contributions may reduce your taxable income

- Investments grow tax-deferred

- Many employers offer matching contributions

- High annual contribution limits

2026 Contribution Limits

- Under age 50: $24,500

- Age 50 and older: Up to $32,500 (including catch-up contributions)

Pros

✔ Immediate tax savings

✔ Employer matching (free money)

✔ Automatic payroll deductions

✔ Higher contribution limits than IRAs

Cons

- Withdrawals in retirement are generally taxed as ordinary income (traditional 401(k)).

- Investment choices are limited to your employer’s plan.

- Required Minimum Distributions (RMDs) may apply after retirement unless rolled into another qualifying account.

What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with after-tax dollars. Although contributions are not tax-deductible, qualified withdrawals in retirement are completely tax-free.

Key Benefits

- Open independently through a financial institution

- Tax-free growth

- Tax-free qualified withdrawals

- No Required Minimum Distributions (RMDs) during the owner’s lifetime

- Excellent for long-term wealth accumulation

2026 Contribution Limits

- Under age 50: $7,500

- Age 50 and older: $8,600

Eligibility to contribute directly to a Roth IRA depends on your modified adjusted gross income (MAGI). Higher-income taxpayers may have reduced contribution limits or may need to consider a Backdoor Roth IRA strategy.

Pros

✔ Tax-free retirement income

✔ No RMDs

✔ Excellent estate planning tool

✔ Flexible withdrawal rules for contributions

Cons

- Contributions are made with after-tax dollars.

- Income limits may restrict eligibility.

- Lower annual contribution limits compared to a 401(k).

What Is a Traditional IRA?

A Traditional IRA is an individual retirement account that may allow tax-deductible contributions depending on your income and participation in an employer-sponsored retirement plan.

Investments grow tax-deferred, but withdrawals in retirement are generally taxable as ordinary income.

2026 Contribution Limits

- Under age 50: $7,500

- Age 50 and older: $8,600

Pros

✔ Potential upfront tax deduction

✔ Tax-deferred investment growth

✔ Wide range of investment options

✔ Easy to open with most financial institutions

Cons

- Withdrawals are taxable in retirement.

- Required Minimum Distributions apply.

- Deductibility may be limited for higher-income taxpayers covered by workplace retirement plans.

Quick Comparison

| Feature | 401(k) | Roth IRA | Traditional IRA |

|---|---|---|---|

| Sponsored By | Employer | Individual | Individual |

| Contributions | Pre-tax (or Roth option if offered) | After-tax | Pre-tax (if deductible) |

| Tax on Withdrawals | Yes (Traditional) | No (qualified withdrawals) | Yes |

| Employer Match | Yes (if offered) | No | No |

| Investment Growth | Tax-deferred | Tax-free | Tax-deferred |

| RMDs | Yes (traditional accounts) | No (Roth IRA) | Yes |

| 2026 Limit | $24,500 ($32,500 age 50+) | $7,500 ($8,600 age 50+) | $7,500 ($8,600 age 50+) |

Which Retirement Account Should You Prioritize?

While every person’s financial situation is different, many financial professionals recommend the following strategy:

Step 1: Contribute Enough to Receive Your Full Employer Match

If your employer offers a matching contribution, contribute at least enough to receive the full match. Employer matching is essentially free money and provides an immediate return on your investment.

Step 2: Maximize Your Roth IRA (If Eligible)

After securing your employer match, consider contributing to a Roth IRA. Tax-free growth and tax-free withdrawals make it one of the most powerful retirement savings vehicles available.

Step 3: Increase Contributions to Your 401(k)

Once your Roth IRA is funded, direct additional retirement savings toward your 401(k), especially if you want to reduce your current taxable income.

Step 4: Consider a Traditional IRA

Depending on your income, tax bracket, and retirement goals, a Traditional IRA may provide additional tax-deferred savings opportunities or be useful as part of a broader retirement strategy.

Factors to Consider Before Choosing

Choosing the right retirement account depends on several factors, including:

- Your current income

- Expected retirement tax bracket

- Employer retirement benefits

- Eligibility for employer matching

- Income limits for Roth IRA contributions

- Desired retirement lifestyle

- Estate planning goals

- Time horizon until retirement

There is no one-size-fits-all solution. A strategy that works for one individual may not be ideal for another.

Common Retirement Planning Mistakes

Many investors unknowingly reduce their long-term retirement potential by making avoidable mistakes.

Missing Employer Matching Contributions

Failing to contribute enough to receive your employer’s full match means leaving free money on the table.

Ignoring Tax Diversification

Relying solely on pre-tax retirement accounts can create higher taxable income during retirement. Maintaining a mix of taxable, tax-deferred, and tax-free accounts provides greater flexibility.

Delaying Retirement Savings

Time is one of the most powerful factors in investing. Starting early allows compound growth to work in your favor.

Not Reviewing Retirement Contributions Annually

Contribution limits often change, and your financial situation evolves over time. Reviewing your retirement strategy each year helps ensure you’re maximizing available opportunities.

Retirement Tax Planning Matters

Building retirement savings is only half the equation. Knowing how and when to withdraw those funds can have a significant impact on your lifetime tax liability.

A comprehensive retirement tax plan should also consider:

- Required Minimum Distributions (RMDs)

- Roth conversion opportunities

- Social Security taxation

- Medicare IRMAA surcharges

- Capital gains planning

- Estate and legacy planning

Strategic tax planning can help you preserve more of your retirement savings and reduce unnecessary taxes throughout retirement.

Schedule Your Retirement Tax Planning Consultation

Whether you’re just beginning to save for retirement or you’re preparing to retire in the next few years, having a personalized tax strategy can help you maximize income and minimize taxes.

At Sure Financial & Tax Services, we provide personalized retirement tax planning designed to help you make informed decisions with confidence.

Our retirement planning services include:

✔ Retirement account strategy

✔ Roth conversion analysis

✔ Social Security tax planning

✔ Required Minimum Distribution (RMD) planning

✔ Retirement income tax projections

✔ Medicare IRMAA planning

✔ Estate and legacy tax strategies

Every retirement journey is unique. Let us help you create a plan that aligns with your financial goals.

Contact Us

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

Maximize Your Retirement Savings. Minimize Taxes. Build a More Secure Financial Future.

Disclaimer: This article is for informational purposes only and should not be considered legal, tax, or investment advice. Consult a qualified tax professional regarding your specific financial situation.