By Surya Padhi, EA, CAA | Sure Financial & Tax Services

Retirement isn’t just about building wealth—it’s about creating a strategy to turn your savings into reliable income while minimizing taxes and preserving your assets for the future.

One of the most overlooked aspects of retirement planning is determining which accounts to withdraw from first. Taking withdrawals in the wrong order can increase taxes, trigger higher Medicare premiums, and reduce the longevity of your retirement portfolio.

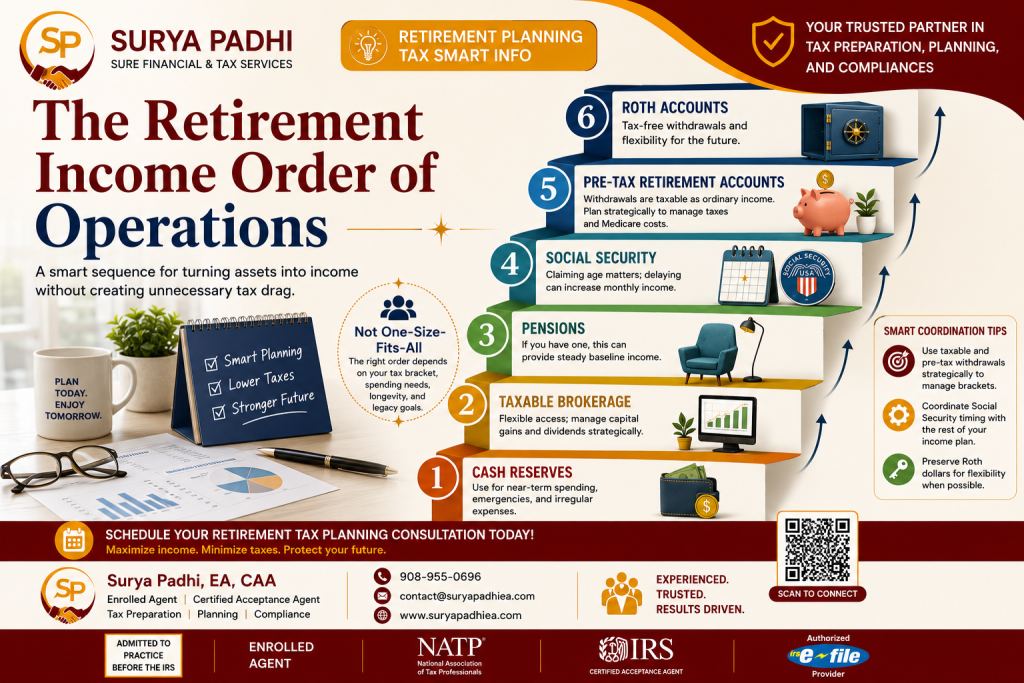

While every retiree’s situation is unique, the following retirement income order of operations provides a framework that many financial and tax professionals use to help retirees maximize after-tax income.

Step 1: Cash Reserves

Your first source of retirement income should often be your cash reserves.

This includes:

- Savings accounts

- Money market accounts

- Emergency funds

- Short-term CDs

Cash reserves are ideal for covering:

- Monthly living expenses

- Unexpected medical bills

- Home repairs

- Market downturns

Why Start Here?

Using cash during volatile market periods allows investment accounts more time to recover and continue growing.

Step 2: Taxable Brokerage Accounts

After cash reserves, many retirees begin drawing from taxable investment accounts.

These may include:

- Individual brokerage accounts

- Mutual funds

- ETFs

- Dividend-paying stocks

Benefits

- Capital gains often receive favorable tax treatment.

- Long-term capital gains tax rates may be lower than ordinary income tax rates.

- Greater flexibility compared to retirement accounts.

Tax Planning Opportunity

Strategically realizing gains can help retirees stay within lower tax brackets and reduce future tax liabilities.

Step 3: Pension Income

For retirees fortunate enough to have a pension, it often serves as a stable income foundation.

Pensions provide:

- Predictable monthly income

- Reduced reliance on investment withdrawals

- Improved retirement cash-flow stability

Planning Consideration

Since pension payments are generally taxable as ordinary income, they should be coordinated with other income sources to manage overall tax exposure.

Step 4: Social Security Benefits

Social Security is one of the most valuable retirement income sources available.

One of the biggest retirement decisions is determining when to claim benefits.

Key Considerations

- Benefits can begin as early as age 62.

- Full Retirement Age depends on your birth year.

- Delaying benefits can increase monthly payments significantly.

Why Timing Matters

For many retirees, delaying Social Security can result in larger guaranteed lifetime income and improved survivor benefits for spouses.

Step 5: Pre-Tax Retirement Accounts

Pre-tax retirement accounts typically include:

- Traditional IRAs

- 401(k)s

- 403(b)s

- SEP IRAs

- SIMPLE IRAs

Withdrawals from these accounts are generally taxed as ordinary income.

Potential Challenges

Large withdrawals can:

- Push retirees into higher tax brackets

- Increase Medicare Part B and Part D premiums

- Cause more Social Security benefits to become taxable

Tax Planning Strategy

Consider:

- Partial Roth conversions

- Strategic withdrawals during low-income years

- Required Minimum Distribution (RMD) planning

Proper coordination can save thousands in lifetime taxes.

Step 6: Roth Accounts

Roth accounts are often considered the most tax-efficient retirement assets.

Examples include:

- Roth IRAs

- Roth 401(k)s

Qualified withdrawals are generally tax-free.

Advantages

- No federal income tax on qualified distributions

- Greater flexibility in retirement

- No lifetime RMDs for Roth IRAs

- Valuable estate planning tool

Why Many Advisors Preserve Roth Assets

Keeping Roth assets for later retirement years provides flexibility when unexpected expenses arise or tax rates increase.

Smart Retirement Income Coordination Tips

Balance Taxable and Tax-Deferred Withdrawals

Rather than draining one account completely before moving to the next, many retirees benefit from coordinating withdrawals across multiple account types.

This approach may help:

- Control tax brackets

- Manage Medicare premiums

- Reduce taxation of Social Security benefits

Coordinate Social Security Timing

The timing of Social Security can significantly affect lifetime retirement income.

A personalized claiming strategy should consider:

- Health

- Life expectancy

- Marital status

- Other retirement assets

Preserve Roth Assets When Possible

Roth accounts provide valuable flexibility because withdrawals generally do not increase taxable income.

Many retirees use Roth assets strategically for:

- Large purchases

- Unexpected healthcare expenses

- Legacy planning

Important: There Is No One-Size-Fits-All Withdrawal Strategy

The ideal retirement income strategy depends on several factors:

- Current tax bracket

- Future tax expectations

- Age

- Health status

- Spending needs

- Medicare considerations

- Estate planning goals

- Legacy objectives

What works for one retiree may be completely inappropriate for another.

How Professional Tax Planning Can Help

Retirement planning is no longer just about investment returns. Today’s retirees must navigate:

- Tax law changes

- Required Minimum Distributions

- Medicare IRMAA surcharges

- Social Security taxation

- Estate planning considerations

A well-designed withdrawal strategy can potentially save tens of thousands of dollars over the course of retirement.

At Sure Financial & Tax Services, we help retirees develop tax-efficient income strategies that align with their financial goals and lifestyle needs.

Schedule a Retirement Tax Planning Consultation

Whether you’re approaching retirement or already retired, we can help you create a personalized withdrawal strategy designed to maximize income and minimize taxes.

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

📧 contact@suryapadhiea.com

🌐 www.suryapadhiea.com

Disclaimer: This article is for educational purposes only and should not be considered personalized tax, legal, investment, or financial advice. Consult a qualified professional regarding your specific circumstances.