By Surya Padhi, EA, CAA | Sure Financial & Tax Services

Building a retirement portfolio is only half the journey. The other half—and arguably the more important part—is knowing how and when to withdraw your retirement savings.

A poorly planned withdrawal strategy can increase your tax bill, trigger higher Medicare premiums, reduce Social Security benefits, and shorten the life of your retirement savings. A tax-efficient withdrawal strategy, on the other hand, can help you maximize after-tax income while preserving your wealth for future generations.

This guide explains the withdrawal rules for four common account types—401(k)s and Traditional IRAs, Roth IRAs, Health Savings Accounts (HSAs), and Taxable Brokerage Accounts—along with best practices to help you make informed retirement decisions.

Why Withdrawal Order Matters

Many retirees focus on how much they’ve saved but overlook the order in which they withdraw funds.

The sequence of withdrawals affects:

- Federal income taxes

- State income taxes

- Medicare IRMAA surcharges

- Taxation of Social Security benefits

- Required Minimum Distributions (RMDs)

- Estate planning and legacy goals

A strategic withdrawal plan can help you keep more of your retirement income and reduce taxes over your lifetime.

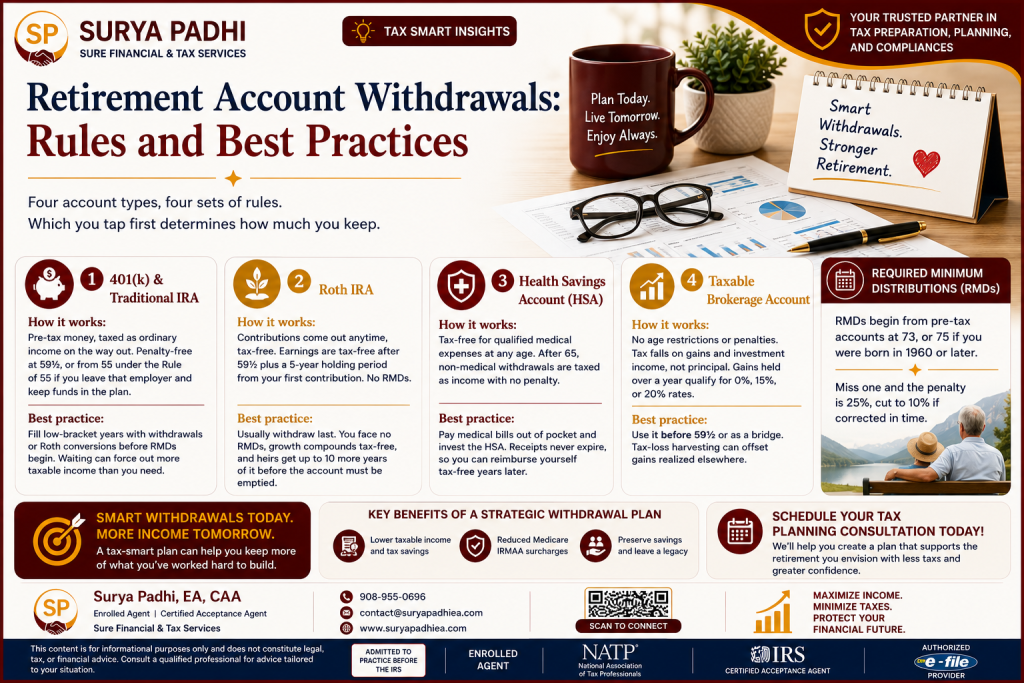

1. 401(k) & Traditional IRA Withdrawals

Traditional 401(k)s and IRAs are funded with pre-tax dollars. While contributions may reduce your taxable income during your working years, withdrawals are generally taxed as ordinary income in retirement.

How It Works

- Contributions may be tax-deductible.

- Investments grow tax-deferred.

- Withdrawals are generally taxable.

- Early withdrawals before age 59½ may be subject to a 10% additional tax unless an exception applies.

Some individuals who leave their employer after age 55 may qualify for the Rule of 55, allowing penalty-free withdrawals from that employer’s 401(k), although ordinary income tax generally still applies.

Best Practices

- Consider taking withdrawals during years when your taxable income is lower.

- Evaluate partial Roth conversions before RMDs begin.

- Coordinate withdrawals with Social Security and other income sources.

- Avoid taking larger distributions than necessary, as they may increase your tax bracket and Medicare premiums.

2. Roth IRA Withdrawals

A Roth IRA is funded with after-tax dollars, making it one of the most tax-efficient retirement accounts available.

How It Works

Qualified withdrawals are generally tax-free if:

- The account has been open for at least five years, and

- You are age 59½ or older (or another qualifying event applies).

Roth IRAs generally do not require Required Minimum Distributions (RMDs) during the original owner’s lifetime.

Best Practices

Many retirees preserve Roth IRA assets for later retirement years because:

- Withdrawals generally do not increase taxable income.

- The account can continue growing tax-free.

- It provides flexibility for unexpected expenses.

- It may offer estate planning advantages for beneficiaries.

3. Health Savings Account (HSA)

An HSA offers one of the most favorable tax treatments available.

Triple Tax Advantage

An HSA may provide:

- Tax-deductible contributions (if eligible)

- Tax-deferred investment growth

- Tax-free withdrawals for qualified medical expenses

This combination is often referred to as the “triple tax advantage.”

After Age 65

After age 65:

- Qualified medical expense withdrawals remain tax-free.

- Non-medical withdrawals are generally taxable as ordinary income but are no longer subject to the additional 20% penalty that typically applies before age 65.

Best Practices

If possible:

- Pay current medical expenses out of pocket.

- Save receipts.

- Allow HSA investments to grow over time.

- Reimburse yourself later for qualified expenses using those saved receipts.

This approach can maximize long-term tax-free growth.

4. Taxable Brokerage Accounts

Taxable investment accounts offer flexibility because there are no age-based withdrawal restrictions.

How It Works

You may owe tax on:

- Capital gains

- Dividends

- Interest income

Long-term capital gains (for assets held more than one year) are generally taxed at favorable rates compared to ordinary income.

Best Practices

Taxable brokerage accounts can be useful:

- Before age 59½ when retirement accounts may have restrictions.

- To bridge income before claiming Social Security.

- To manage taxable income strategically.

- For tax-loss harvesting opportunities that may offset capital gains.

Understanding Required Minimum Distributions (RMDs)

Federal law requires many retirees to begin taking Required Minimum Distributions (RMDs) from certain retirement accounts once they reach the applicable age.

Generally:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- Traditional 401(k)s

are subject to RMD rules.

Roth IRAs owned by the original account holder generally are not subject to lifetime RMDs.

Missing an RMD can result in significant IRS penalties, although penalties may be reduced if corrected promptly under current law.

Common Retirement Withdrawal Mistakes

Many retirees unintentionally increase their lifetime tax bill by making avoidable mistakes.

Waiting Too Long to Withdraw from Pre-Tax Accounts

Delaying withdrawals until RMDs begin may result in larger mandatory distributions later, increasing taxable income.

Draining One Account Before Another

Withdrawing from only one account type without considering taxes can lead to unnecessary tax costs.

Ignoring Roth Conversion Opportunities

Years with lower taxable income may present opportunities to convert portions of traditional retirement accounts to Roth accounts.

Overlooking Medicare Premiums

Higher taxable income can increase Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amounts (IRMAA).

Not Coordinating with Social Security

The timing of retirement account withdrawals can affect how much of your Social Security benefits become taxable.

Sample Retirement Withdrawal Strategy

Consider a retiree with:

- Taxable brokerage account

- Traditional IRA

- Roth IRA

- HSA

One possible approach might include:

- Use taxable investments strategically for early retirement income.

- Withdraw from Traditional IRAs in lower-tax years while managing tax brackets.

- Preserve Roth IRA assets for flexibility and later retirement needs.

- Use HSA funds for qualified medical expenses when appropriate.

The optimal sequence depends on your income needs, tax situation, age, and long-term objectives.

Frequently Asked Questions

Should I withdraw from my Roth IRA first?

In many cases, retirees choose to preserve Roth IRA assets because qualified withdrawals are generally tax-free and the account is not subject to lifetime RMDs. However, the best strategy depends on your individual circumstances.

Are all retirement withdrawals taxable?

No. Tax treatment depends on the account type. Traditional retirement accounts are generally taxable, while qualified Roth IRA withdrawals are generally tax-free.

Can I access retirement funds before age 59½?

Possibly. Certain exceptions, such as the Rule of 55 for eligible employer plans and other IRS exceptions, may allow penalty-free withdrawals. Income tax may still apply.

Should I work with a tax professional before taking retirement withdrawals?

Yes. Coordinating withdrawals with Social Security, Medicare, capital gains, and Required Minimum Distributions can help reduce taxes and preserve retirement savings.

Schedule Your Retirement Tax Planning Consultation

Retirement withdrawal decisions can affect your taxes for decades. A personalized strategy can help you maximize after-tax income while preserving your wealth.

Whether you’re approaching retirement or already retired, we can help you create a customized withdrawal strategy that aligns with your financial goals.

Our retirement planning services include:

✔ Tax-efficient withdrawal planning

✔ Roth conversion analysis

✔ Required Minimum Distribution (RMD) planning

✔ Social Security tax planning

✔ Medicare IRMAA planning

✔ Retirement income projections

✔ Estate and legacy planning

Contact Us Today

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

Maximize Retirement Income. Minimize Taxes. Protect Your Financial Future.

Schedule your retirement tax planning consultation today and gain confidence in every withdrawal decision.