By Surya Padhi, EA, CAA | Sure Financial & Tax Services

Giving to charity is one of the most meaningful ways to support the causes you care about. But did you know that with proper planning, charitable giving can also reduce your tax bill?

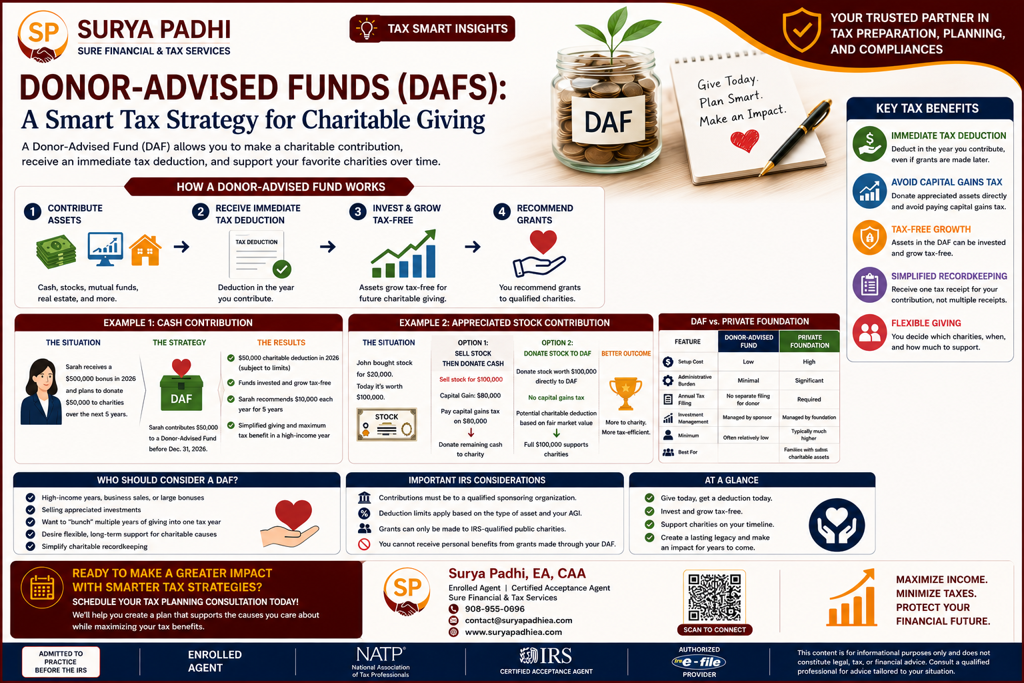

A Donor-Advised Fund (DAF) is one of the fastest-growing charitable giving tools in the United States. It allows you to make a charitable contribution, receive an immediate tax deduction, and distribute grants to your favorite charities over time.

Whether you’re selling a business, exercising stock options, receiving a large bonus, or simply looking to maximize your charitable impact, a Donor-Advised Fund can be an effective tax planning strategy.

What Is a Donor-Advised Fund?

A Donor-Advised Fund (DAF) is a charitable investment account established through a sponsoring organization, such as a community foundation or financial institution.

You contribute cash or appreciated assets into the fund and receive an immediate charitable tax deduction. The assets can then be invested and grow tax-free while you recommend grants to qualified charities whenever you’re ready.

Think of a DAF as a “charitable savings account.”

How Does a Donor-Advised Fund Work?

The process is straightforward:

Step 1: Contribute Assets

You can donate:

- Cash

- Publicly traded stocks

- Mutual funds

- ETFs

- Cryptocurrency (through some sponsors)

- Privately held business interests (subject to sponsor approval)

- Real estate (with some sponsoring organizations)

Step 2: Receive an Immediate Tax Deduction

You generally receive a charitable deduction in the year you contribute the assets—even if the money isn’t distributed to charities until years later.

Step 3: Invest the Assets

The funds can be invested in various portfolios and grow tax-free, potentially increasing the amount available for future charitable grants.

Step 4: Recommend Grants

Over time, you recommend grants from your DAF to IRS-qualified charitable organizations.

The sponsoring organization reviews the request and distributes the funds.

Example: How a Donor-Advised Fund Can Save Taxes

Scenario

Sarah receives a $500,000 year-end bonus in 2026. She also plans to donate $50,000 to several charities over the next five years.

Instead of writing checks to charities each year, she contributes $50,000 to a Donor-Advised Fund before December 31, 2026.

Results

- She receives a $50,000 charitable deduction on her 2026 tax return (subject to IRS deduction limits).

- The funds are invested and have the opportunity to grow tax-free.

- Over the next five years, Sarah recommends annual grants of $10,000 to her favorite charities.

- She avoids the administrative burden of tracking multiple donations each year.

This strategy allows Sarah to maximize her tax deduction in a high-income year while supporting charitable causes over time.

Example: Donating Appreciated Stock

Suppose John purchased stock several years ago for $20,000. Today, it’s worth $100,000.

If John sells the stock:

- Capital Gain: $80,000

- Potential federal capital gains tax applies.

Instead, John donates the stock directly to a Donor-Advised Fund.

Potential Benefits

✔ No capital gains tax on the appreciated stock (if donated directly).

✔ Potential charitable deduction based on the fair market value of the stock, subject to IRS rules.

✔ The full value can be used to support charities.

This strategy can be significantly more tax-efficient than selling the stock first and donating the cash.

Key Tax Benefits of a Donor-Advised Fund

Immediate Tax Deduction

You generally receive a deduction in the year you contribute assets to the fund, even if grants are made later.

Avoid Capital Gains Tax

Contributing appreciated securities directly to a DAF may allow you to avoid paying capital gains tax on the appreciation.

Tax-Free Investment Growth

Assets inside the DAF can be invested and potentially grow tax-free, increasing your charitable impact.

Simplified Recordkeeping

Instead of collecting receipts from multiple charities throughout the year, you’ll typically receive a single tax acknowledgment for your DAF contribution.

Flexible Giving

You decide:

- Which charities receive grants

- When grants are made

- How much each charity receives

This allows you to plan your charitable giving strategically.

Who Should Consider a Donor-Advised Fund?

A DAF may be especially beneficial if you:

- Have a high-income year.

- Sell a business.

- Receive a large bonus or commission.

- Exercise stock options.

- Sell appreciated investments.

- Want to “bunch” multiple years of charitable giving into one tax year.

- Wish to simplify charitable recordkeeping.

- Plan to make long-term philanthropic contributions.

Donor-Advised Fund vs. Private Foundation

| Feature | Donor-Advised Fund | Private Foundation |

|---|---|---|

| Setup Cost | Low | High |

| Administrative Burden | Minimal | Significant |

| Annual Tax Filing | No separate filing for the donor | Required |

| Investment Management | Managed by sponsoring organization | Managed by the foundation |

| Minimum Contribution | Often relatively low | Typically much higher |

| Best For | Most individual donors | Families with substantial charitable assets |

For many taxpayers, a Donor-Advised Fund offers similar charitable benefits with much lower cost and complexity than establishing a private foundation.

Important IRS Considerations

While Donor-Advised Funds offer significant tax advantages, there are important rules to remember:

- Contributions must be made to a qualified sponsoring organization.

- Deduction limits vary depending on the type of asset donated and your adjusted gross income (AGI).

- Grants can generally only be made to IRS-qualified public charities.

- You cannot receive personal benefits from grants made through your DAF.

Because the rules can be complex, it’s important to consult a qualified tax professional before making large charitable contributions.

Frequently Asked Questions

Can I donate appreciated stock?

Yes. Donating appreciated securities directly to a Donor-Advised Fund can be one of the most tax-efficient ways to give.

Can I make anonymous donations?

Yes. Many sponsoring organizations allow grants to be made anonymously if desired.

Can my family help manage the fund?

Many Donor-Advised Funds allow spouses, children, or successor advisors to recommend grants, making them a valuable tool for family philanthropy.

Is there a minimum contribution?

Minimum contributions vary by sponsoring organization. Some providers allow accounts to be opened with relatively modest initial contributions.

Is a Donor-Advised Fund Right for You?

A Donor-Advised Fund is not just for wealthy individuals. It can benefit anyone who wants to combine charitable giving with smart tax planning.

If you’re anticipating a high-income year or have appreciated investments, a DAF may help you:

- Reduce your taxable income

- Avoid capital gains tax on donated assets

- Simplify charitable giving

- Support the causes you care about for years to come

Schedule a Tax Planning Consultation

If you’re considering a Donor-Advised Fund, selling appreciated assets, or looking for tax-efficient charitable giving strategies, we can help evaluate whether a DAF fits into your overall financial plan.

At Sure Financial & Tax Services, we work with individuals, families, retirees, and business owners to develop personalized tax strategies that align with their financial and charitable goals.

Our services include:

✔ Charitable Giving Tax Planning

✔ Capital Gains Tax Strategies

✔ Retirement Tax Planning

✔ Year-End Tax Planning

✔ Business Tax Planning

✔ Investment Tax Planning

✔ Individual & Business Tax Preparation

Contact Us Today

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

Give Smarter. Save More. Make a Lasting Impact.

Schedule your consultation today and discover how strategic charitable planning can help you maximize both your tax savings and your philanthropic legacy.

Disclaimer

This article is for informational purposes only and should not be considered legal, tax, or financial advice. Tax rules governing charitable contributions and Donor-Advised Funds are subject to IRS limitations and individual circumstances. Consult a qualified tax professional before implementing any charitable giving strategy.