Surya Padhi, EA, CAA | Sure Financial & Tax Services

Most tax refunds happen for one reason: too much money was withheld from your paycheck throughout the year. While getting a refund may feel like a bonus, it often means you gave the IRS an interest-free loan.

On the other hand, withholding too little can result in an unexpected tax bill, penalties, and financial stress when filing your return.

The key is finding the right balance.

This guide explains how to determine whether your paycheck withholding is on track for 2026 and what steps you can take to avoid surprises at tax time.

Why Paycheck Withholding Matters

Federal income taxes are generally paid throughout the year through payroll withholding. Your employer uses the information on your Form W-4 to estimate how much federal income tax should be withheld from each paycheck.

If your withholding is:

Too High

- You receive a large tax refund.

- Your monthly cash flow is reduced.

- The government holds your money interest-free.

Too Low

- You may owe taxes when filing your return.

- You could be subject to IRS underpayment penalties.

- Budgeting becomes more difficult.

The goal is not necessarily to receive a large refund. The goal is to have your withholding closely match your actual tax liability.

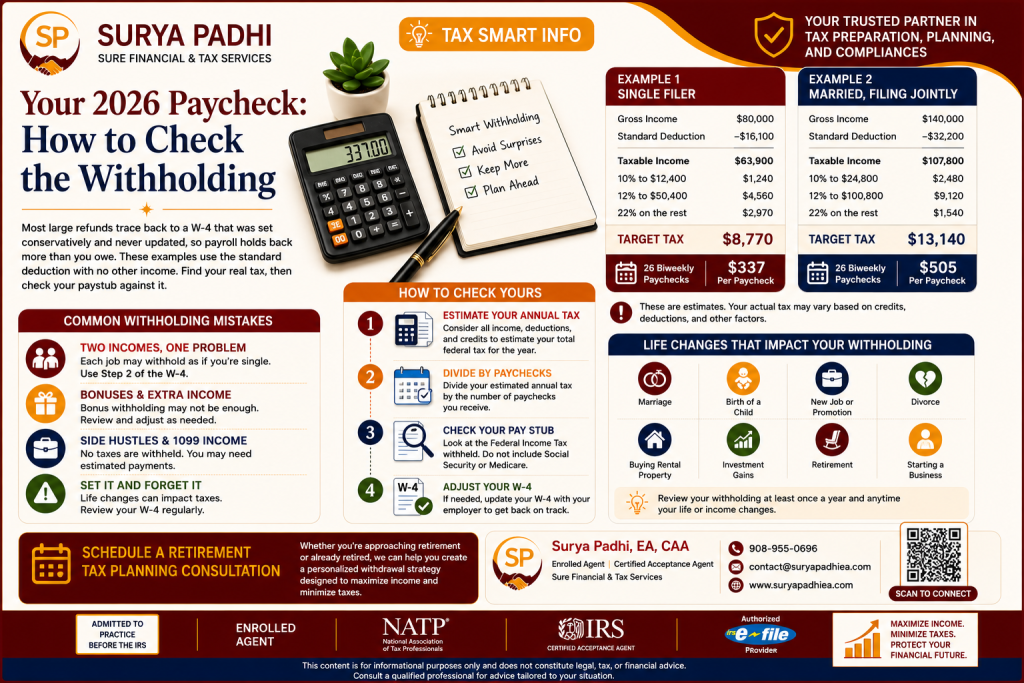

Example 1: Single Filer

Assume the following:

| Description | Amount |

|---|---|

| Gross Income | $80,000 |

| Standard Deduction | $16,100 |

| Taxable Income | $63,900 |

Estimated Federal Tax

| Tax Bracket | Tax |

|---|---|

| 10% on first $12,400 | $1,240 |

| 12% on next $50,400 | $6,048 |

| 22% on remaining income | $330 |

| Target Federal Tax | Approximately $7,618 |

If you receive 26 biweekly paychecks, your withholding should average roughly:

$7,618 ÷ 26 = $293 per paycheck

Example 2: Married Filing Jointly

Assume:

| Description | Amount |

|---|---|

| Gross Income | $140,000 |

| Standard Deduction | $32,200 |

| Taxable Income | $107,800 |

Estimated Federal Tax

| Tax Bracket | Tax |

|---|---|

| 10% on first $24,800 | $2,480 |

| 12% on next $83,000 | $9,960 |

| Target Federal Tax | Approximately $12,440 |

With 26 paychecks, withholding should average approximately:

$12,440 ÷ 26 = $478 per paycheck

How to Check Your Withholding

Step 1: Estimate Your Annual Tax

Consider:

- Salary

- Bonuses

- Investment income

- Rental income

- Business income

- Tax credits

- Deductions

The more accurate your estimate, the more precise your withholding adjustment will be.

Step 2: Divide by Number of Paychecks

Take your estimated annual tax and divide it by the number of pay periods during the year.

For example:

$8,770 ÷ 26 paychecks = $337 withheld per paycheck

This gives you a benchmark for comparison.

Step 3: Review Your Pay Stub

Locate the line labeled:

Federal Income Tax

Do not include:

- Social Security tax

- Medicare tax

- State withholding

- Local withholding

Compare your actual federal withholding to your target amount.

Step 4: Adjust Your W-4 if Necessary

If your withholding is too low or too high, submit a revised Form W-4 to your employer.

Even a small adjustment today can prevent a large tax bill later.

Common W-4 Mistakes

Married Couples with Two Incomes

One of the most common reasons taxpayers owe money is because both spouses work.

Each employer typically calculates withholding as if that employee is the household’s only source of income.

This often leads to under-withholding.

Solution

Complete Step 2 of Form W-4 to account for multiple jobs or a working spouse.

Receiving Bonuses

Bonus income can increase your tax liability significantly.

Common examples include:

- Annual bonuses

- Sales commissions

- Stock awards

- Restricted Stock Units (RSUs)

Many employees discover that withholding on bonus payments is not enough to cover the actual tax due.

Side Hustles and Self-Employment Income

Income reported on:

- Form 1099-NEC

- Form 1099-K

- Form 1099-MISC

typically has no federal tax withholding.

If you earn freelance, consulting, rideshare, or online business income, additional withholding or quarterly estimated payments may be required.

Life Changes That Require a W-4 Review

You should review your withholding whenever you experience:

- Marriage

- Divorce

- Birth of a child

- New job

- Promotion

- Significant raise

- Retirement

- Rental property income

- Investment gains

- Self-employment income

These events often change your overall tax liability.

Why a Mid-Year Tax Review Is Important

Waiting until tax season to discover withholding issues leaves little opportunity to fix them.

A mid-year tax review can help you:

✔ Prevent IRS penalties

✔ Increase take-home pay

✔ Reduce unexpected tax bills

✔ Improve cash flow

✔ Identify tax-saving opportunities

✔ Prepare for year-end planning

For many taxpayers, a simple withholding adjustment can save thousands of dollars in future tax surprises.

Frequently Asked Questions

Is a large refund a good thing?

Not necessarily. A large refund often means you had too much tax withheld during the year.

How often should I review my W-4?

At least once annually and whenever you experience a significant life or income change.

Can I change my W-4 anytime?

Yes. Employees can submit an updated W-4 to their employer at any time.

What if my spouse and I both work?

Dual-income households often need additional withholding adjustments using Step 2 of Form W-4.

Should retirees review withholding?

Absolutely. Pension income, IRA distributions, Social Security benefits, and investment income can all affect tax liability.

Tax Planning Tip

The best time to fix withholding problems is before year-end.

By reviewing your paycheck today, you can make adjustments that reduce tax surprises, improve cash flow, and keep your financial goals on track.

A proactive tax strategy helps ensure you’re paying the right amount throughout the year—not too much and not too little.

Schedule a Retirement Tax Planning Consultation

Whether you’re approaching retirement or already retired, we can help you create a personalized withdrawal strategy designed to maximize income and minimize taxes.

Our retirement and tax planning services can help you:

✔ Develop a tax-efficient withdrawal strategy

✔ Reduce taxation of Social Security benefits

✔ Evaluate Roth conversion opportunities

✔ Manage Required Minimum Distributions (RMDs)

✔ Coordinate pension, IRA, and investment income

✔ Minimize Medicare IRMAA surcharges

✔ Preserve wealth for future generations

Every retirement plan is unique. A customized strategy can help you keep more of your retirement savings and enjoy greater financial confidence.

Contact Us Today

Surya Padhi, EA, CAA

Enrolled Agent | Certified Acceptance Agent

Sure Financial & Tax Services

📞 908-955-0696

Maximize Income. Minimize Taxes. Protect Your Financial Future.

Schedule your consultation today and discover how proactive tax planning can help you keep more of what you earn and save.